Smart Capital News

April 2, 2026

Smart Capital News

April 2, 2026

According to Q1 2026 mortgage application fraud data, multifamily and investment property loans remain the highest-risk categories for document fraud — with an estimated 1 in 26 applicationscontaining indicators of misrepresentation. Generative AI has made fabricating supporting documentation a matter of minutes, rendering traditional manual review processes structurally unable to keeppace. For lenders and investors still relying on periodic document checks, the gap between what borrowers submit and what is actually true has never been wider or harder to close.

This analysis draws on Smart Capital Center — a CRE AI platform processing $500B+ in analyzed transactions across 120M+ properties, trusted by institutional lenders and investors includingKeyBank, JLL, and The RMR Group — to map exactly how AI-powered fraud detection works across the commercial real estate lending and investment lifecycle.

“Fraud Alerts is the result of two years of focused collaboration with lenders and mortgage professionals who wanted a better way to detect risks hidden within borrower reporting. Through continuous feedback, testing, and real-world use cases, we developed an AI capability specifically built for CRE finance, combining financial analysis, document intelligence, and underwriting workflows into a unified risk detection system,” said Laura Krashakova, CEO of Smart Capital Center.

AI fraud detection in CRE refers to the continuous, automated analysis of borrower-submitted financial and operational property data to identify inconsistencies, anomalies, and patterns that indicatereporting errors, operational risk, or intentional misrepresentation.

Unlike manual document review — which is periodic, analyst-dependent, and limited to what a single reviewer can cross-reference at once — AI fraud detection operates continuously across alldocuments simultaneously, comparing data points across sources and time periods to surface discrepancies that human review would miss.

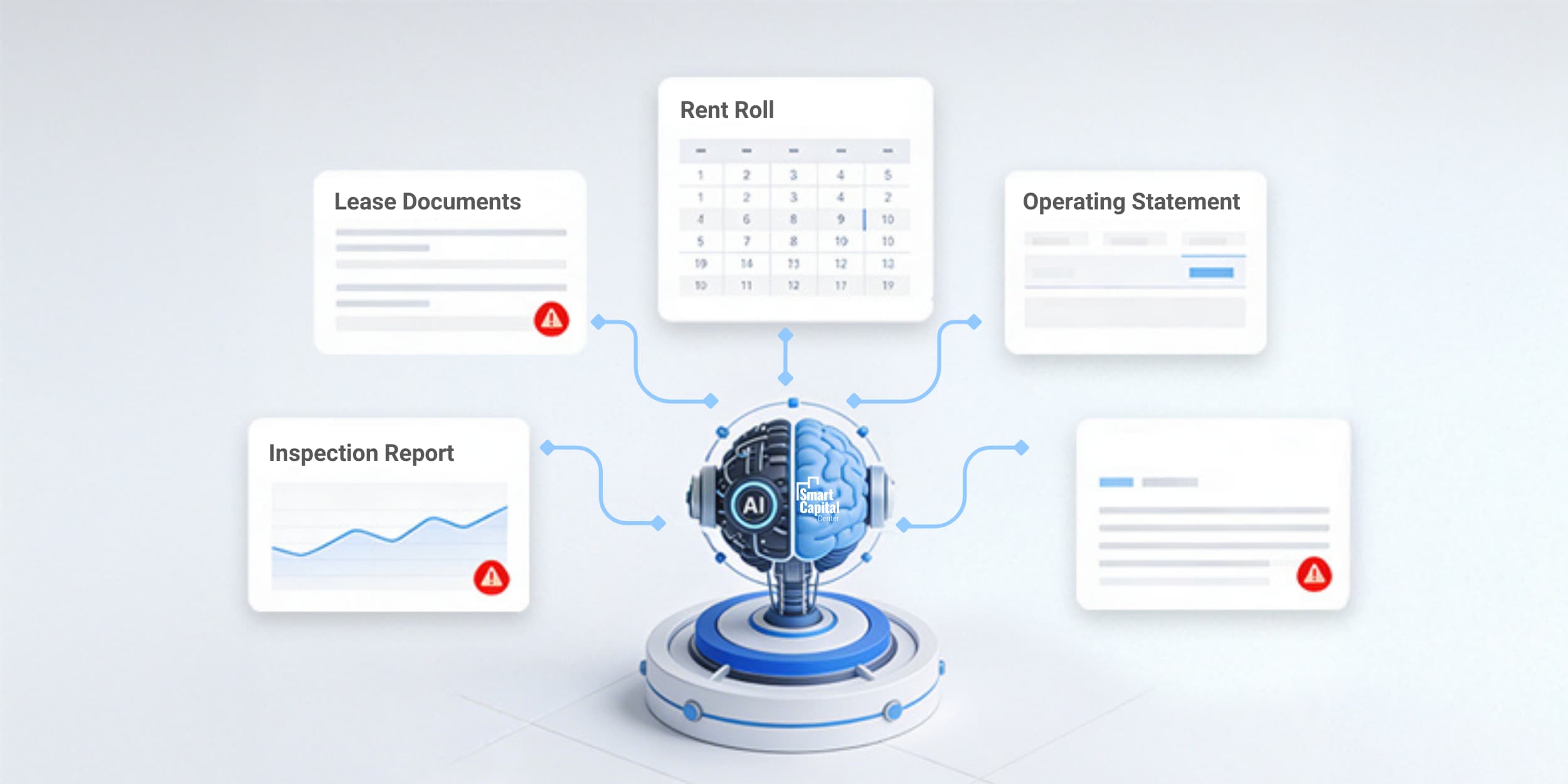

Smart Capital Center's Fraud Alerts capability functions as an AI-driven digital auditor: ingesting rent rolls, operating statements, lease records, and financial reports, then cross-referencing themagainst each other and against real-time market data to flag patterns that warrant investigation. Every alert includes a direct link to the underlying source documents, a side-by-side variance report, and a full audit trail — giving analysts the evidence they need to investigate, escalate, or dismiss each finding with confidence.

Fraud Alerts was developed in direct collaboration with leading multifamily lenders over two years of real-world testing and feedback, built specifically for the document complexity and fraud typologiesthat define CRE finance, not adapted from a generic financial services tool.

.jpg)

The Scale of the Problem: Why Manual Review Can No Longer Protect Lenders

The fraud risk facing CRE lenders in 2026 is not a marginal compliance concern. It is a systemic operational threat — and the numbers reflect it.

The U.S. Department of Justice recently indicted four individuals and the real estate investment group Vision & Beyond Group LLC in connection with a $50 million bank fraud conspiracy — alleging thatdefendants falsified financial documents, altered closing materials, and removed mortgagees from title commitments to conceal refinancing fraud across approximately 100 multifamily properties. Thiscase is not an outlier. It is a documented example of the fraud typology that AI detection is purpose-built to surface.

Major industry participants — including Freddie Mac and Fannie Mae — have elevated fraud prevention to a strategic priority, hosting a series of lender education roundtables through the MortgageBankers Association specifically focused on detection and prevention. Laura Krashakova, CEO of Smart Capital Center, addressed this systemic risk at MBA CREF 2026, where the topic generatedsignificant discussion among lenders, investors, and technology providers.

"Generative AI makes it possible to fabricate financial documents in minutes," Krashakova noted during her address. "Numbers can be modified to appear plausible, supporting documentation can be generated instantly, and entire borrower narratives can be constructed artificially. The process is faster and the results more convincing than anything a manual reviewer can reliably distinguish."

The core vulnerability is structural: CRE lenders receive financial data from multiple sources — rent rolls, operating statements, appraisals, inspection reports — and those sources are rarely reconciledagainst each other in real time. This fragmentation is where fraud hides.

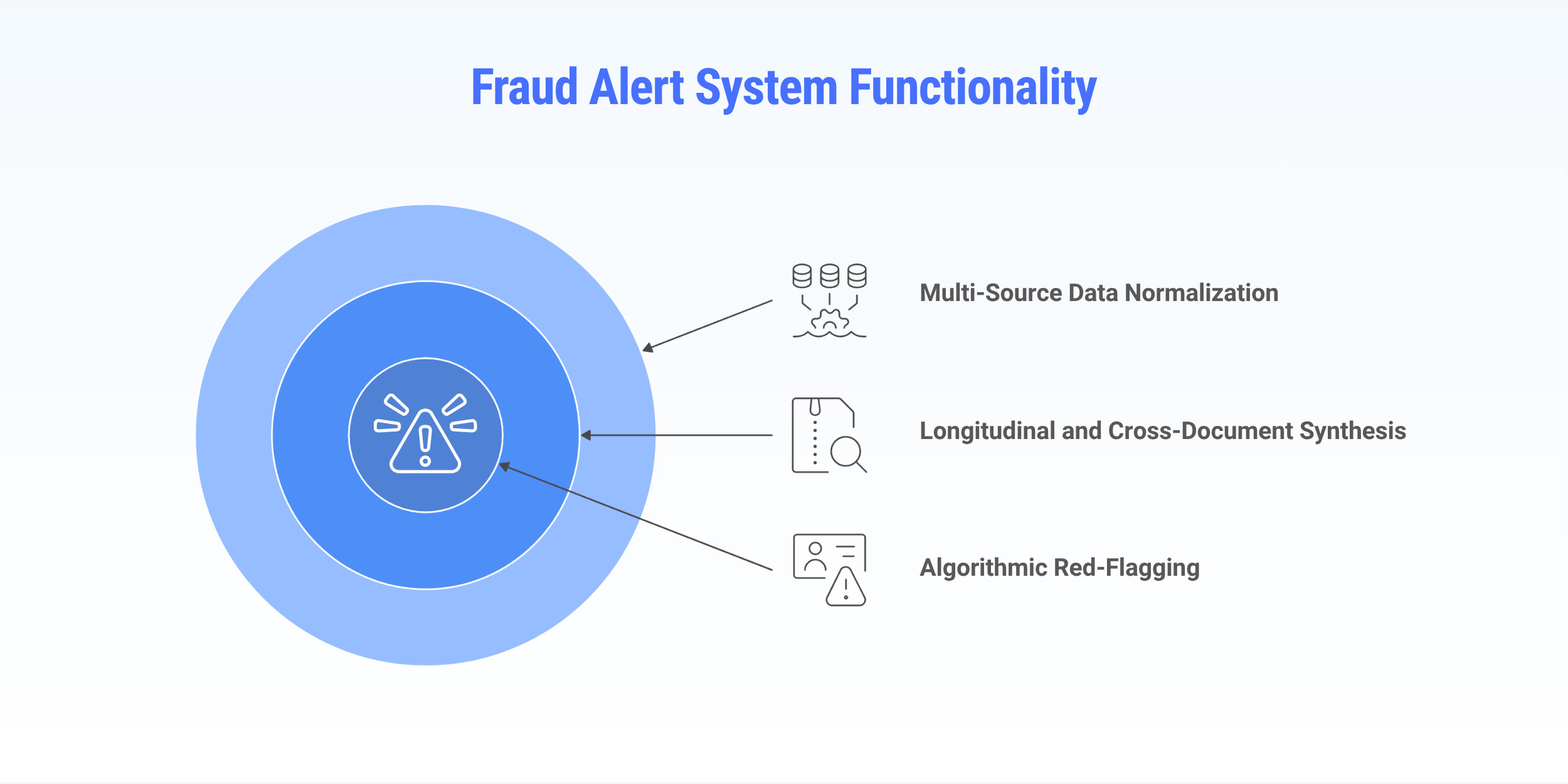

How AI Fraud Detection Works: The Three-Layer Framework

Smart Capital Center's Fraud Alerts capability applies three sequential analytical layers to every document submitted across the loan lifecycle.

The Technical Framework: How Fraud Alerts Work

Smart Capital Center’s Fraud Alerts capability functions as an AI-driven digital auditor, continuously analyzing financial and operational property data to identify suspicious patterns and reporting inconsistencies.

The system evaluates large volumes of information across documents and time periods, identifying anomalies that may otherwise remain hidden during manual review processes.

1. Multi-Source Data Normalization

Commercial real estate transactions depend on borrower-provided documents that arrive in inconsistent formats — complex Excel spreadsheets, scanned PDFs, unstructured operating statements — often at different stages of the loan lifecycle. The platform ingests all file types and converts them into a uniform digital structure, enabling apples-to-apples comparison across thousands of line itemsregardless of how each document was originally formatted.

2. Longitudinal and Cross-Document Synthesis

Once normalized, the AI analyzes data across two dimensions that manual review cannot reach at scale. Horizontally, it cross-references documents from the same reporting period — comparing a rent roll against an operating statement to verify that revenue totals and occupancy metrics are consistent. Longitudinally, it tracks the same data points over time — identifying when lease expiration dates, rent figures, or occupancy rates shift between reporting periods without corresponding documentation to explain the change.

3. Algorithmic Red-Flagging

When the synthesis layer identifies a pattern that exceeds risk thresholds, the system generates a structured alert — categorized by fraud typology, linked to the underlying source documents, and accompanied by a side-by-side variance report. Alerts can be prioritized for immediate committee attention, dismissed when a discrepancy is verified as legitimate, and annotated with investigationnotes that become part of the asset's permanent digital record.

Five Fraud Typologies AI Catches Before Loan Review Is Complete

The following five scenarios reflect real fraud patterns detected through AI analysis. Each represents a category of misrepresentation that manual periodic review consistently misses.

Phantom Occupancy — Vacant Units Reporting as Occupied

The scenario: A borrower submits quarterly financials for a 300-unit multifamily asset showing 95% occupancy — meeting the minimum DSCR covenant threshold.

What the AI found: Cross-referencing the granular rent roll against a recent inspection report, the system flagged that 15 "occupied" units were dark and vacant. The summary page occupancy figure had been calculated to meet the covenant, not to reflect actual conditions.

Why it matters for lenders: A DSCR calculated on phantom occupancy overstates the loan's collateral quality. Catching this at the quarterly review rather than at annual renewal saved the lender froma covenant breach that would have required workout intervention.

WALT Manipulation — Inflated Lease Terms to Justify Acquisition Pricing

The scenario: An acquisitions manager evaluates a $50M office asset. The seller's data room reflects a long Weighted Average Lease Term (WALT), suggesting low rollover risk at the acquisitionprice.

What the AI found: Longitudinal analysis revealed that lease expiration dates for the three largest anchor tenants had shifted forward by 24 months compared to rent rolls from the prior year — with no executed lease amendments in the data room to support the extensions. The updated figures reflected projected renewals, not signed ones.

Why it matters for investors: An acquisition priced on a fabricated WALT exposes the buyer to concentrated rollover risk the underwriting model did not reflect. Re-negotiating the purchase pricebased on the actual, shorter lease terms directly protected the firm's projected IRR.

Revenue Mismatch — Ancillary Income Bundled into Base Rent

The scenario: A loan servicing manager receives monthly "rent roll vs. P&L" updates across a 500-loan multifamily portfolio. The fund's underwriting guidelines exclude ancillary income — storagefees, commercial parking — from DSCR calculations.

What the AI found: A revenue mismatch alert flagged a suburban asset where total rent on the operating statement was significantly higher than total residential rent on the rent roll. The borrower hadbundled $12,000 in storage locker fees and commercial signage rent into the "Base Rent" line item — artificially inflating the property's DSCR against the covenant threshold.

Why it matters for lenders: This is not fraud in the criminal sense — it is a reporting methodology inconsistency that, left undetected, would have produced an inaccurate covenant pass. AI catches itbecause it compares every line item across every document, not just summary figures.

Short-Term Masking — Unauthorized Short-Term Rentals Hiding Declining Demand

The scenario: A senior portfolio manager oversees a high-end urban multifamily portfolio. A borrower submits an annual rent roll showing exceptional market rents and 98% occupancy — significantlyoutperforming the local submarket despite a general cooling trend.

What the AI found: Cross-referencing the submitted rent roll against external market data and real-time listings, the system identified that reported market rents were 15% above the actual long-termrates for the zip code. Further investigation revealed that a significant share of "occupied" units were being rented on unauthorized short-term leases — generating a temporary revenue spike thatmasked declining long-term demand and real occupancy risk.

Why it matters for investors: Valuing an asset on inflated short-term revenue overstates its stabilized NOI and leads to over-leveraging against a property whose true performance is declining. Adjusting the valuation to stabilized residential rents corrected the risk exposure before the position was sized.

CapEx Diversion — Renovation Funds Redirected to Cover Operating Deficits

The scenario: An asset manager monitors a value-add bridge loan for a 200-unit garden-style apartment. The underwritten pro forma assumed a $2 million renovation plan designed to justify a $250/month rent premium per unit post-renovation.

What the AI found: A stagnant rent growth alert and a CapEx utilization anomaly triggered simultaneously. Cross-referencing the borrower's submitted draws against the rent roll, the AI identified thatdespite 75% of the renovation budget being marked as spent, collected rents for the units remained at pre-renovation levels. Inspection reports confirmed no physical modernization had beenperformed. Loan proceeds were being redirected to cover operational deficits at another of the borrower's properties.

Why it matters for lenders: Draw diversion in construction and value-add loans is among the most financially damaging fraud typologies — because the collateral value the lender underwrote nevermaterializes. Catching this mid-draw cycle allows for a notice of default and halt on further funding before total collateral loss occurs.

.jpg)

CapEx Diversion — Renovation Funds Redirected to Cover Operating Deficits

The scenario: An asset manager monitors a value-add bridge loan for a 200-unit garden-style apartment. The underwritten pro forma assumed a $2 million renovation plan designed to justify a $250/month rent premium per unit post-renovation.

What the AI found: A stagnant rent growth alert and a CapEx utilization anomaly triggered simultaneously. Cross-referencing the borrower's submitted draws against the rent roll, the AI identified thatdespite 75% of the renovation budget being marked as spent, collected rents for the units remained at pre-renovation levels. Inspection reports confirmed no physical modernization had beenperformed. Loan proceeds were being redirected to cover operational deficits at another of the borrower's properties.

Why it matters for lenders: Draw diversion in construction and value-add loans is among the most financially damaging fraud typologies — because the collateral value the lender underwrote nevermaterializes. Catching this mid-draw cycle allows for a notice of default and halt on further funding before total collateral loss occurs.

Risks of Not Implementing AI Fraud Detection

A fraud detection capability is not just a risk management investment — it is a competitive and regulatory necessity. Lenders and investors operating without continuous AI monitoring face specific, quantifiable risks.

Examiner findings on monitoring gaps. Regulatory examiners from the OCC and FDIC increasingly cite inadequate loan monitoring documentation as a deficiency in CRE portfolio reviews. Periodicmanual review cycles that cannot demonstrate real-time surveillance of covenant compliance and borrower reporting create examination exposure that is separate from the fraud risk itself.

AI-generated documents that pass visual review. The sophistication of AI-fabricated financial documents in 2026 has reached the point where altered rent rolls, modified operating statements, and manipulated loan-to-value calculations are visually indistinguishable from legitimate materials. Manual review by experienced analysts is no longer a reliable control — the detection gap is structural, nota training problem.

Concentration risk that surfaces too late. Portfolio-level fraud patterns — multiple borrowers using the same fabrication methodology, concentrated DSCR manipulation across a specific asset class— are invisible when each loan is reviewed individually. AI detects cross-portfolio patterns that no single analyst monitoring individual positions could identify.

Mitigation: Smart Capital Center's Fraud Alerts addresses all three risks through continuous monitoring, cross-document synthesis, and portfolio-wide anomaly detection — with a full audit trail thatsatisfies examiner documentation requirements on every position simultaneously.

How to Evaluate an AI Fraud Detection Platform for CRE

Not all fraud detection tools are built for the document complexity and fraud typologies specific to commercial real estate. When evaluating platforms, apply this framework:

Step 1: Test cross-document reconciliation on a real asset. Upload a rent roll, operating statement, and inspection report from the same period for a property in your current portfolio. Confirm theplatform cross-references all three — not just processes each document individually. A system that analyzes documents in isolation will miss the mismatch patterns where fraud hides.

Step 2: Verify longitudinal analysis capability. Submit two rent rolls from the same asset six months apart and confirm the platform identifies changes in lease terms, expiration dates, or occupancyfigures without supporting amendment documentation. Static document analysis cannot catch WALT manipulation or short-term masking — only time-series comparison can.

Step 3: Confirm alert traceability to source documents. Every alert should link directly to the underlying clause, line item, or document that triggered it. If the platform surfaces a revenue mismatchbut cannot show you exactly which line item on which document caused the discrepancy, the alert is not actionable.

Step 4: Assess the audit trail for regulatory compliance. Confirm that all alert actions — prioritization, dismissal, investigation notes — are permanently recorded with timestamps and userattribution. This documentation is what satisfies OCC and FDIC examination requirements for demonstrated monitoring activity.

Step 5: Evaluate portfolio-level aggregation. A fraud detection system that operates loan by loan cannot identify cross-portfolio patterns. Confirm the platform surfaces anomalies across your entireloan book simultaneously — not just within individual positions.

Smart Capital Center's Fraud Alerts is built to pass all five tests — with continuous cross-document synthesis, full longitudinal tracking, source-level audit trails, and portfolio-wide pattern detectionacross every position simultaneously.

Conclusion

AI-generated document fraud is not a future risk — it is the current operating environment for every CRE lender and investor processing borrower-submitted financial data in 2026. The fraud typologiesare specific and repeatable: phantom occupancy, WALT manipulation, revenue mismatch, short-term masking, and CapEx diversion are not theoretical vulnerabilities. They are documented patternsthat AI detection surfaces and manual review consistently misses.

The lenders and investors that implement continuous AI monitoring today are not just managing fraud risk more effectively — they are building the institutional data infrastructure that separatesdefensible underwriting from exposure they cannot see. As Krashakova concluded at MBA CREF 2026: "In a world where fraud is increasingly automated, the only effective defense is equallysophisticated intelligence."

Discover how Smart Capital Center is reshaping the future of CRE finance.

Frequently Asked Questions

How can I tell if a borrower has submitted fraudulent documents in a CRE loan application?

The most reliable detection method is cross-document reconciliation — comparing the rent roll against the operating statement, the operating statement against inspection reports, and currentdocuments against prior-period submissions. Discrepancies that a borrower cannot explain with supporting documentation are the primary signal of misrepresentation. AI platforms like Smart Capital Center perform this reconciliation automatically across all submitted documents simultaneously, flagging anomalies with direct links to the underlying source data so your team can investigate ratherthan search.

What types of CRE fraud does AI detect that manual review typically misses?

AI excels at detecting fraud patterns that require cross-referencing multiple data points across documents and time periods — which is exactly what manual periodic review cannot do at scale. The mostcommon typologies: phantom occupancy (vacant units reported as occupied), WALT manipulation (lease expiration dates updated without signed amendments), revenue mismatch (ancillary incomebundled into base rent to inflate DSCR), short-term masking (unauthorized short-term leases hiding declining long-term demand), and CapEx diversion (renovation draws spent on operating deficits at other properties). Each requires comparison across multiple documents or reporting periods to detect — a structural advantage of continuous AI analysis over periodic human review.

How does AI fraud detection help me meet OCC and FDIC examination requirements for CRE loan monitoring?

Regulatory examiners require evidence of continuous, documented loan monitoring — not just periodic review records. Smart Capital Center's Fraud Alerts generates a permanent audit trail of allmonitoring activity: every alert triggered, every investigation note added, every alert prioritized or dismissed, with timestamps and user attribution. This documentation demonstrates active, real-time surveillance to examiners in a format that satisfies CRE concentration monitoring expectations without requiring additional analyst hours to compile.

Can AI detect draw fraud in construction and value-add loans before additional funding is released?

Yes — draw fraud detection is one of the highest-value applications of AI in CRE lending. Smart Capital Center's draw reconciliation capability cross-references funding requests against approvedbudget line items, completion percentage certifications, and inspection reports. A CapEx utilization anomaly — where reported spend significantly exceeds the physical improvements documented in inspection records — triggers an alert before the next draw is released, giving the lender the evidence needed to pause funding, request documentation, or issue a notice of default.

How long does it take to implement AI fraud detection across an existing loan portfolio?

Smart Capital Center clients typically begin receiving Fraud Alerts within weeks of onboarding — the platform ingests existing loan documents, rent rolls, and operating statements and begins cross-referencing immediately. For portfolios with historical reporting data, the longitudinal analysis capability activates as soon as prior-period documents are uploaded, enabling detection of pattern changesthat predate the implementation date. Most lenders see the first portfolio-wide anomaly surfaced within the first reporting cycle after deployment.

.jpg)